Living with chronic obstructive pulmonary disease (COPD) can make it hard to breathe, work, and manage everyday tasks. If your condition is severe enough to keep you from earning a living, you may be entitled to disability benefits under one or more Canadian federal programs — but the application process is rarely straightforward.

This guide explains what COPD is, whether it can qualify for Canada Pension Plan (CPP) Disability benefits and the Disability Tax Credit (DTC), what other conditions like osteoarthritis may also qualify, and what practical steps you can take to strengthen your claim. Whether you are just starting to research your options or you have already received a denial, understanding your rights is the first step.

If you would like a plain-English overview of how the program works and what you could be entitled to, visit our CPP Disability practice page or try our free CPP disability calculator to get an initial sense of your potential monthly benefit.

Table of Contents

- What Is COPD?

- Does COPD Qualify for Disability in Canada?

- What Benefits Can I Get If I Have COPD?

- COPD and the Disability Tax Credit

- What Is the $40,000 Disability Grant?

- Does Osteoarthritis Qualify for Disability in Canada?

- How to Build a Strong CPP Disability Claim for COPD or Osteoarthritis

What Is COPD?

Chronic obstructive pulmonary disease (COPD) is an umbrella term for a group of progressive lung diseases — most commonly emphysema and chronic bronchitis — that cause airflow obstruction and make breathing increasingly difficult over time.

COPD is typically staged from mild (Stage I) to very severe (Stage IV) using a measurement called FEV1 (forced expiratory volume in one second), which tracks how much air you can forcefully exhale. As the disease advances, symptoms such as chronic cough, excess mucus, wheezing, and shortness of breath on exertion become more limiting.

COPD is largely caused by long-term exposure to lung irritants — cigarette smoke is the most common, but occupational dust, chemical fumes, and air pollution also play a role. While COPD has no cure, treatments including bronchodilators, corticosteroids, pulmonary rehabilitation, and in some cases supplemental oxygen can slow its progression and manage symptoms.

For disability purposes, what matters is not simply the diagnosis but the functional impact the disease has on your ability to work and carry out daily activities. A Stage II COPD patient who manages symptoms well may still hold full-time employment; a Stage III or IV patient may find that even walking short distances or climbing stairs triggers severe breathlessness.

Does COPD Qualify for Disability in Canada?

Yes — COPD can qualify for disability in Canada, but eligibility depends on the severity of your condition and the specific program you are applying to.

CPP Disability Benefits

The Canada Pension Plan (CPP) Disability program, administered by Service Canada, is the largest federal income-replacement program for people with disabilities. To qualify, you must meet two core tests:

- Contribution test — You must have made sufficient CPP contributions in recent years (generally four of the last six years, or three of the last six if you have 25+ years of contributions).

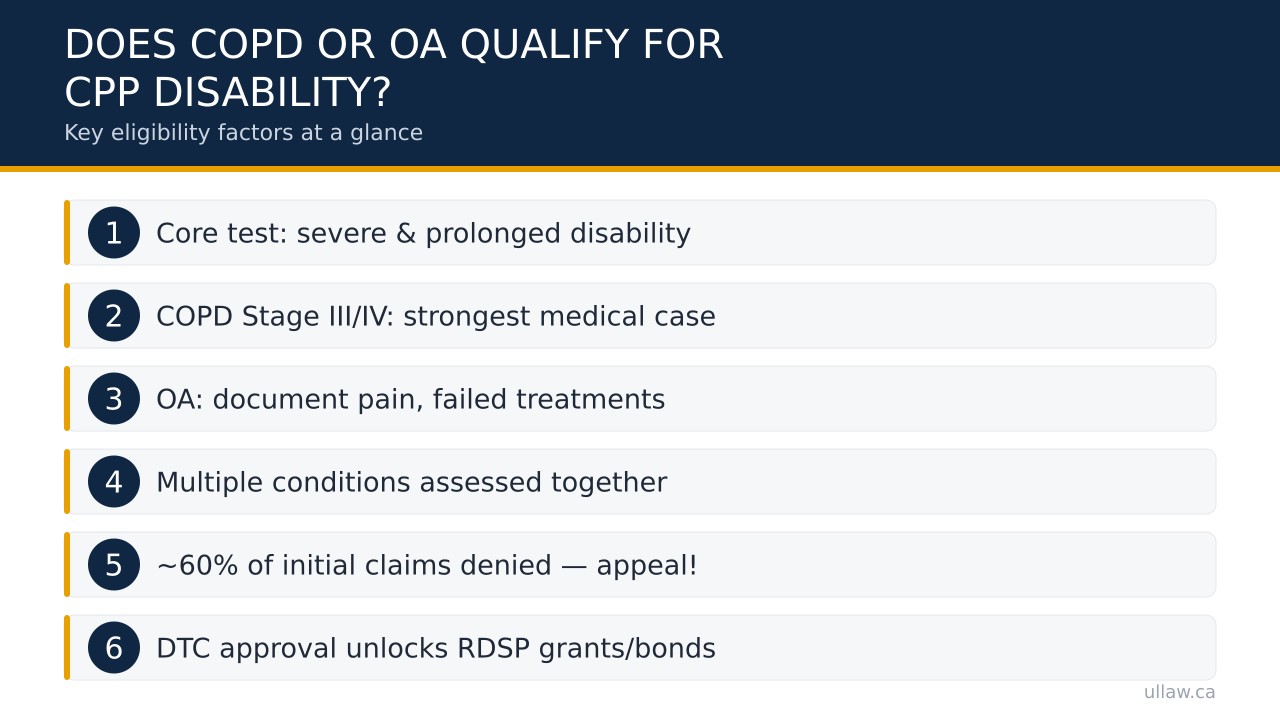

- Medical test — Your disability must be severe and prolonged. “Severe” means you are regularly incapable of pursuing any substantially gainful occupation. “Prolonged” means the condition is long-term or likely to result in death.

COPD itself does not automatically satisfy the medical test — what matters is functional capacity. At advanced stages (Stage III or IV), COPD frequently causes breathlessness at rest or with minimal exertion, chronic fatigue, and recurrent respiratory infections that collectively can make any sustained employment impossible. When objective evidence such as pulmonary function tests, arterial blood gas results, and your treating physician’s clinical notes all support severe functional limitation, a CPP Disability claim for COPD has a solid medical foundation.

Mobility Limitations Related to COPD

COPD’s impact extends beyond the lungs. Severe breathlessness restricts how far you can walk, how long you can stand, and how much physical effort you can sustain. Many claimants also experience:

- Hypoxia-related cognitive fog that impairs concentration and memory

- Anxiety and depression triggered by the fear of breathlessness

- Musculoskeletal deconditioning from reduced activity

- Sleep disturbances from nocturnal oxygen desaturation

These secondary effects can be just as disabling as the primary breathing limitation and should be fully documented in your medical records and any supporting reports from specialists such as respirologists or occupational therapists.

What Stage of COPD Qualifies for Disability?

There is no single stage that automatically qualifies. That said, applicants with Stage III (severe) or Stage IV (very severe) COPD — where FEV1 falls below 50% of predicted — are most likely to satisfy the CPP Disability “severe and prolonged” standard, particularly when combined with frequent exacerbations and documented inability to sustain work activity. Earlier-stage COPD combined with other serious conditions (heart disease, diabetes, mental health disorders) may also cumulatively meet the threshold. Always have your full medical picture assessed.

What Benefits Can I Get If I Have COPD?

Canadians living with COPD may be eligible for several overlapping programs. Here is a summary of the most relevant ones:

1. CPP Disability Benefit

A monthly taxable benefit paid to eligible contributors who can no longer work due to a severe and prolonged disability. The amount depends on your CPP contribution history. Use our CPP disability calculator for a personalised estimate.

2. Disability Tax Credit (DTC)

A non-refundable federal tax credit that reduces income tax payable for people with severe and prolonged impairments in physical or mental functions. For COPD, eligibility typically hinges on whether you are markedly restricted in a basic activity of daily living — most commonly breathing or walking. A qualified practitioner (usually your respirologist or family physician) must certify your limitations on the DTC application form. Learn more through Canada Revenue Agency’s official guidance.

3. Registered Disability Savings Plan (RDSP)

Once approved for the DTC, you become eligible for the Registered Disability Savings Plan, a long-term savings vehicle that may attract the Canada Disability Savings Grant and the Canada Disability Savings Bond from the federal government. This is the program sometimes referred to in connection with amounts up to $40,000 in lifetime government contributions (grants and bonds combined can be substantial over time — the exact amounts depend on your income, contribution history, and the year contributions are made).

4. Employment Insurance Sickness Benefits

If your COPD temporarily prevents you from working, you may qualify for EI sickness benefits through Service Canada for up to 26 weeks, provided you have enough insurable hours.

5. Provincial Disability Assistance

Ontario’s Ontario Disability Support Program (ODSP) can provide income and employment support to residents whose disability substantially restricts their ability to work. Details are available through the Ontario government’s website.

6. Long-Term Disability (LTD) Insurance

If you have group or individual LTD coverage through an employer or association, your policy may provide income replacement — typically 60–70% of pre-disability earnings — subject to its own definition of disability.

COPD and the Disability Tax Credit

The Disability Tax Credit (DTC) is often the gateway to other federal programs, including the RDSP and the Child Disability Benefit. For a COPD patient, the most relevant DTC categories are:

- Breathing — You may qualify if you take three times longer than an average person to perform the mental or physical tasks related to breathing, or if you require life-sustaining therapy (such as supplemental oxygen for more than 14 hours per day).

- Walking — Severe COPD that restricts you to walking very short distances may qualify under the walking category.

- Cumulative effect of significant limitations — Even if no single function meets the threshold alone, restrictions across multiple categories can cumulatively qualify.

How Hard Is It to Get Approved for the DTC?

Approval rates vary. The CRA reviews both the medical certificate completed by your practitioner and, sometimes, additional questionnaires. COPD claims are more likely to succeed when:

- Objective test results (spirometry, six-minute walk tests) clearly reflect severe limitation

- Your practitioner provides specific, detailed descriptions of functional restriction — not just a diagnosis

- The cumulative effects of COPD alongside other conditions are fully captured

A denial is not the end of the road. You have the right to request an informal review and ultimately to appeal to the Tax Court of Canada. Legal assistance at the appeals stage can significantly change the outcome in complex cases. Our team at UL Lawyers can guide you through the CPP Disability and DTC processes.

What Is the $40,000 Disability Grant?

You may have seen references online to a $40,000 disability grant — this figure relates to the Canada Disability Savings Grant (CDSG) and the Canada Disability Savings Bond (CDSB), which are federal government contributions to an RDSP.

Here is how it works in brief:

- CDSG: The government matches RDSP contributions at rates of up to 300% on the first $500 contributed and 200% on the next $1,000, depending on family income. Maximum grant per year is $3,500; maximum lifetime grant is $70,000.

- CDSB: Lower-income Canadians with disabilities may receive up to $1,000 per year in bond contributions, with a lifetime maximum of $20,000, even with no personal contribution required.

The “$40,000” figure sometimes cited is an informal shorthand — the actual amounts you could receive depend on your income, age, contribution history, and how long the RDSP has been open. You must be approved for the DTC to open an RDSP. For official details, consult Canada Revenue Agency’s RDSP guidance.

Does Osteoarthritis Qualify for Disability in Canada?

Yes — osteoarthritis can qualify for disability in Canada, including for CPP Disability benefits and the DTC, depending on its severity and functional impact.

Osteoarthritis (OA) is the most common form of arthritis. It involves the breakdown of cartilage in joints — most frequently the knees, hips, hands, and spine — causing pain, stiffness, swelling, and reduced range of motion. It is a leading cause of disability in Canadians over 50.

CPP Disability and Osteoarthritis

As with COPD, a diagnosis of osteoarthritis alone does not guarantee approval. The CPP Disability adjudicator focuses on whether your condition renders you regularly incapable of any substantially gainful occupation. Factors that strengthen an OA disability claim include:

- Documented severity: imaging (X-rays, MRI) showing advanced joint deterioration; specialist reports from rheumatologists or orthopaedic surgeons

- Failed conservative treatment: evidence that physiotherapy, medications, injections, and other interventions have not adequately restored function

- Surgical history: prior joint replacements that have not resolved functional limitations

- Pain assessments: consistent, objectively supported records of severe chronic pain

- Functional limitations: inability to sit, stand, walk, or use hands/fingers for extended periods — all of which are critical for most forms of employment

Osteoarthritis and the Disability Tax Credit

OA claimants most often qualify under the walking or dressing categories of the DTC, or cumulatively across multiple basic activities of daily living. As with COPD, detailed functional descriptions from your physician or specialist are essential.

When OA and COPD Co-Exist

Many Canadians live with both COPD and osteoarthritis simultaneously — a combination that can compound functional limitations far beyond what either condition causes alone. A CPP Disability adjudicator is required to consider your overall medical picture, not each diagnosis in isolation. If you have multiple conditions, make sure every one is documented and reported in your application.

How to Build a Strong CPP Disability Claim for COPD or Osteoarthritis

Whether your disabling condition is COPD, OA, or a combination of both, the foundation of a successful claim is the same: thorough, consistent, and objective medical documentation.

Key Steps

-

See your specialist regularly — Gaps in medical records are one of the most common reasons for denial. Regular appointments with a respirologist (for COPD) or rheumatologist/orthopaedic surgeon (for OA) create a clear trail of your condition’s progression.

-

Ask your doctor to document function, not just diagnosis — “Patient has COPD” is much weaker than “Patient is unable to walk more than 50 metres without severe dyspnoea and must rest for 20 minutes before resuming activity.”

-

Complete the application forms carefully — The CPP Disability application includes both a self-reported questionnaire and a medical report. Both matter. Underreporting your limitations on a bad day can harm your claim.

-

Don’t ignore secondary conditions — Anxiety, depression, sleep apnoea, and musculoskeletal deconditioning are all potentially relevant. List every diagnosed condition.

-

Appeal if denied — Approximately 60% of initial CPP Disability applications are denied, but many are successfully overturned at the reconsideration and Social Security Tribunal stages. A denial letter is not the final word.

-

Get legal help early — An experienced disability lawyer can identify gaps in your file before you submit, not just after a denial. Visit our CPP Disability practice page to learn how we can help, and use our CPP disability calculator to estimate your potential benefit amount.

For official eligibility criteria and application forms, see Service Canada’s CPP Disability page and the Ontario e-Laws database for relevant provincial legislation.

Talk to a UL Lawyers Team Member

If COPD, osteoarthritis, or another serious condition is preventing you from working, you may have more options than you realise — and more to lose by waiting. The team at UL Lawyers offers a free, no-obligation consultation to review your situation and explain exactly where you stand. Reach out today and let us help you take the next step with confidence.