Finding out the driver who just hit you has no insurance can feel like the ground dropping out from under you. Your car is damaged, you may be hurt, and the person responsible can’t pay. It is a frightening situation — but it is not a dead end.

Ontario’s auto insurance system has several overlapping safety nets designed for exactly this scenario. Your own insurance policy almost certainly contains protections you may not even know you have, including coverage for accidents caused by uninsured and unidentified (“hit-and-run”) drivers. On top of that, a provincial fund of last resort exists for those who have no insurance of their own.

This guide walks you through every recovery avenue available to you, explains how the OPCF-44R endorsement works, and tells you what steps to take right now to protect your claim. If you want to understand what your case might be worth, try our personal injury settlement calculator — and when you’re ready to talk to a lawyer, our motor vehicle accident legal team offers free consultations.

Table of Contents

- What Happens If the At-Fault Driver Is Uninsured in Ontario?

- Understanding Ontario’s Mandatory Auto Insurance Laws

- What Is the OPCF-44R Endorsement and How Does It Protect You?

- What Is the Motor Vehicle Accident Claims Fund?

- What Happens When You Are Hit by a Hit-and-Run Driver?

- Consequences for Driving Without Insurance in Ontario

- How an At-Fault Accident Affects Your Insurance — Even If the Other Driver Was Uninsured

- Steps to Take After Being Hit by an Uninsured Driver

- How Much Compensation Can You Recover?

- Why Legal Representation Matters in Uninsured Driver Claims

What Happens If the At-Fault Driver Is Uninsured in Ontario?

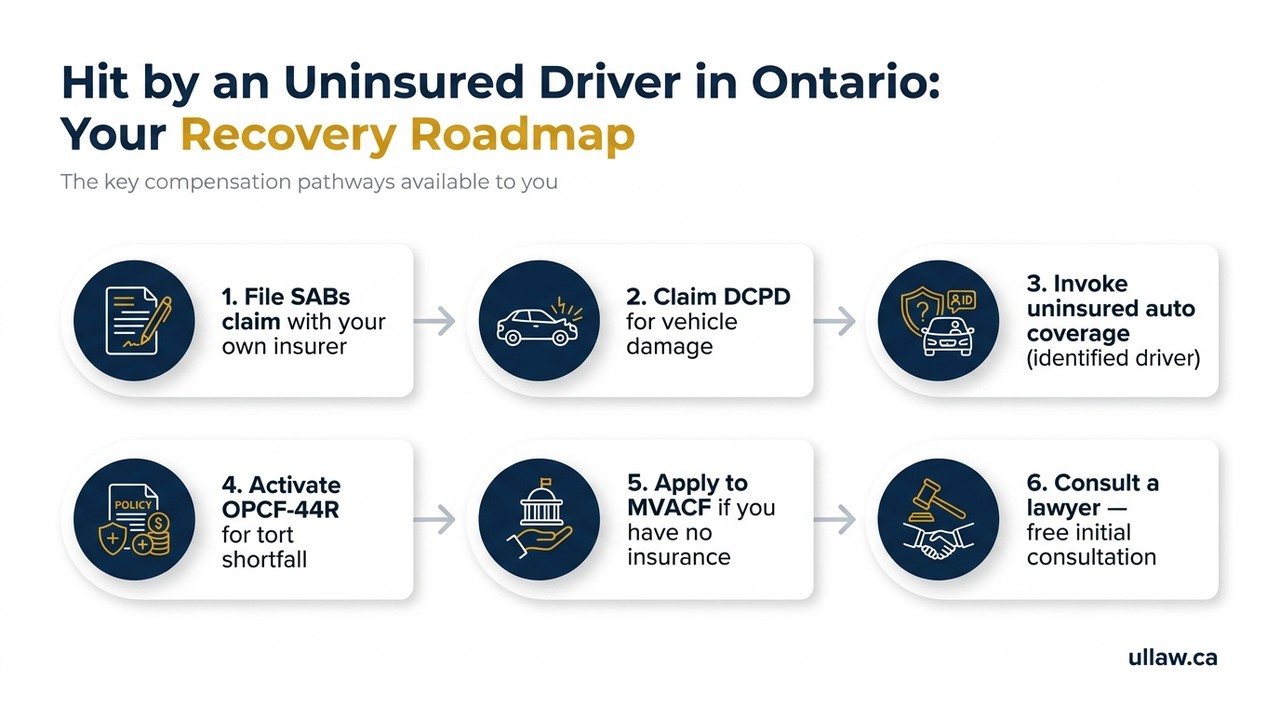

When the driver who caused your accident has no valid auto insurance, your options depend on two things: whether the at-fault driver has been identified, and what coverage you carry on your own policy.

If the at-fault driver is known but uninsured

You can still sue that driver personally for damages. The problem is obvious — an uninsured driver often has limited assets, so a judgment against them may be difficult to collect on. That is why your own policy’s protections become critical.

Direct Compensation – Property Damage (DCPD) covers damage to your vehicle when an identified, at-fault driver is involved, even if that driver is uninsured, as long as the collision occurred in Ontario. Under Ontario’s Insurance Act, every standard auto policy includes DCPD, so your own insurer steps in to repair or replace your vehicle (minus your deductible).

For bodily injury compensation, you would look first to your Statutory Accident Benefits (SABs) — income replacement, medical and rehabilitation benefits, and attendant care — which your insurer must provide regardless of who caused the crash. For pain-and-suffering damages and other tort losses beyond SABs, you would pursue the at-fault driver directly. If they cannot pay, the OPCF-44R endorsement (explained in depth below) may top up what you can recover.

If the at-fault driver fled the scene (hit-and-run / unidentified driver)

If you never got a plate number and cannot identify the driver, you are dealing with an unidentified motorist scenario. Your own policy’s uninsured automobile coverage — a mandatory component of every Ontario policy under the Insurance Act — kicks in. You must report the collision to police and to your insurer promptly. There is also a rule that physical contact between vehicles must generally have occurred (independent witness evidence can sometimes substitute — speak to a lawyer about your specific facts).

The bottom line

Being hit by an uninsured driver does not mean you walk away empty-handed. Ontario’s insurance framework is designed so that innocent victims have a path to compensation even when the wrongdoer cannot pay.

Understanding Ontario’s Mandatory Auto Insurance Laws

Ontario law requires every vehicle driven on a public road to carry third-party liability insurance of at least $200,000. This requirement is set out in the Insurance Act and enforced by the province. Yet despite the legal obligation, a meaningful number of drivers remain uninsured — whether because they let a policy lapse, never obtained coverage, or deliberately chose to drive without it.

Every standard Ontario auto policy — called an OAP 1 (Owner’s Policy) — automatically includes:

- Third-party liability (minimum $200,000)

- Statutory Accident Benefits (SABs)

- Direct Compensation – Property Damage (DCPD)

- Uninsured automobile coverage

These are not optional add-ons. They are the legislated baseline. The uninsured automobile section is what protects you when the other driver has no coverage at all — and it is mandatory in every policy sold in Ontario.

Additionally, drivers may purchase the OPCF-44R Family Protection Endorsement, which significantly expands the amount recoverable in an uninsured or underinsured driver scenario. More on that in the next section.

What Is the OPCF-44R Endorsement and How Does It Protect You?

The OPCF-44R Family Protection Endorsement is an optional add-on to an Ontario auto policy, but it is one of the most valuable coverages you can buy — and it is surprisingly affordable.

What it does

OPCF-44R protects you and your family members (including household residents and occupants of your vehicle) when the at-fault driver is either:

- Uninsured (no insurance at all), or

- Underinsured (their liability limit is lower than the damages you suffered)

It effectively bridges the gap between what you can recover from the at-fault driver’s insurance (if any) and your own policy’s liability limit.

Example: Suppose your damages are assessed at $500,000, but the at-fault driver carried only the minimum $200,000 in liability coverage. Without OPCF-44R, you could be left $300,000 short. With OPCF-44R (typically written at $1 million or $2 million), your own insurer covers the shortfall up to your endorsement limit.

Who is covered

- The named insured

- Spouse and dependent relatives living in the household

- Any person who was an occupant of your insured vehicle at the time of the crash

What OPCF-44R does NOT do

- It is not a standalone policy — you must have an underlying OAP 1

- It does not create a double recovery; amounts received from the at-fault driver’s insurer are deducted

- It has its own claims process and deadlines — typically you must notify your insurer in writing within a set period after the accident

If you are unsure whether your policy includes OPCF-44R, check your Declaration Page or call your broker. If you do not have it, speak to your broker about adding it — the additional premium is modest given the protection it provides.

What Is the Motor Vehicle Accident Claims Fund?

What if you have no auto insurance of your own and you are hit by an uninsured or unidentified driver? Ontario’s insurer of last resort is the Motor Vehicle Accident Claims Fund (MVACF).

Administered by the province under the Insurance Act, MVACF was created to ensure that innocent accident victims are not left entirely without recourse simply because neither party had insurance.

Who can claim from MVACF

You may be eligible if:

- You were injured in an Ontario motor vehicle accident

- The at-fault driver is uninsured or unidentified

- You do not have your own auto insurance policy through which to claim

If you do have your own insurance, you must first exhaust that coverage before turning to MVACF.

What MVACF covers

- Statutory Accident Benefits (income replacement, medical/rehab, attendant care, etc.)

- Bodily injury damages (pain and suffering, loss of income)

- Property damage in limited circumstances

Important limitations

MVACF claims involve the provincial government as the responding party, and the process can be slower and more adversarial than a standard insurer claim. There are strict notice and limitation period requirements. Benefit levels follow the same SABs framework as a standard policy, but the overall claims experience is different.

For anyone navigating an MVACF claim, legal advice is strongly recommended. Visit the Ontario government’s website for general information on the fund, and speak with a personal injury lawyer about your specific situation.

What Happens When You Are Hit by a Hit-and-Run Driver?

A hit-and-run — where the at-fault driver flees before being identified — is treated as an unidentified motorist claim under Ontario law. The process differs slightly from an uninsured (but identified) driver scenario.

Steps to take immediately

- Call 911 and report the collision. A police report is critical and, under your policy, likely required.

- Gather witness information. Independent witnesses who saw the other vehicle can be vital for establishing that physical contact occurred, which most policies require.

- Document the scene. Photographs, dashcam footage, and any debris from the other vehicle can support your claim.

- Notify your insurer promptly. Most policies require notice within a very short window — often within 24 hours or as soon as reasonably possible.

- Seek medical attention. Even if you feel fine, symptoms of soft-tissue injuries and concussion can appear days later. A medical record establishes the link to the accident.

The physical contact requirement

Ontario’s mandatory uninsured automobile coverage traditionally requires that there was physical contact between your vehicle and the unidentified vehicle. Courts have recognized that this rule can produce harsh results in cases where a driver swerves to avoid an unidentified vehicle and crashes. If your situation involves no physical contact, you should speak with a lawyer immediately — the law in this area is nuanced and your facts matter.

OPCF-44R and hit-and-run

If you carry the OPCF-44R endorsement, it also responds to unidentified motorist scenarios, potentially increasing the compensation available to you beyond the base uninsured automobile coverage limits.

Consequences for Driving Without Insurance in Ontario

It is worth understanding the penalties that face the uninsured driver — both because it affects how they behave after a crash and because it contextualizes why Ontario has built alternative compensation systems.

Fines and licence consequences

Under the Compulsory Automobile Insurance Act, driving without valid insurance in Ontario carries:

- First offence: fines ranging from $5,000 to $25,000

- Subsequent offences: fines up to $50,000

- Licence suspension of up to one year

- Vehicle impoundment for up to three months

These are among the stiffest traffic penalties in Ontario.

Can you go to jail for driving without insurance in Ontario?

A conviction under the Compulsory Automobile Insurance Act is a provincial offence, not a criminal offence under the Criminal Code of Canada. Jail is not a prescribed penalty for simply driving without insurance. However, if the uninsured driver also committed other offences in connection with the accident — such as dangerous driving, impaired driving, or fleeing the scene — those can carry Criminal Code consequences including imprisonment.

What if YOU were uninsured when the crash occurred?

If you were driving without insurance and were injured in an accident you did not cause, you may still have access to Statutory Accident Benefits through the at-fault driver’s insurer or through MVACF — but your tort claim for pain and suffering may be significantly compromised. Ontario courts and insurers treat an uninsured victim’s claim differently, and you should get legal advice as soon as possible.

How an At-Fault Accident Affects Your Insurance — Even If the Other Driver Was Uninsured

A common concern after any collision is: will this affect my insurance rates?

When you are the innocent victim

If the other driver was entirely at fault, claiming under your own policy — including under the uninsured automobile or OPCF-44R provisions — should generally not be treated as an at-fault claim on your record. Ontario’s Direct Compensation – Property Damage rules and the standard DCPD claims process are designed so that innocent claimants are protected from premium increases for not-at-fault accidents.

However, the practical reality is that your premium can still be affected depending on your insurer and your policy terms. Some insurers may adjust premiums upon renewal even for not-at-fault claims. Ask your broker about your Accident Forgiveness endorsement if you have one — it may prevent a first not-at-fault claim from impacting your rate.

How long does an at-fault accident affect your insurance in Ontario?

For a genuinely at-fault accident, Ontario insurers typically record it on your insurance history for six years. During that period, the at-fault accident can factor into your premium calculation, especially in the first three years. An uninsured or not-at-fault accident should not appear as an at-fault conviction on your record, but the accident itself may appear as a claims history entry.

The practical takeaway

Always ask your insurer or broker exactly how a claim will be coded before you file — and do not let fear of a premium increase stop you from making a legitimate claim for injuries. The value of proper compensation almost always outweighs a modest rate adjustment.

Steps to Take After Being Hit by an Uninsured Driver

Acting quickly and strategically in the hours and days after the crash can make the difference between a strong claim and a compromised one.

Immediately at the scene

- Call 911. Report the accident and request police attendance, especially if the other driver admits to having no insurance.

- Exchange information. Even without insurance, get the other driver’s name, address, driver’s licence number, and vehicle plate.

- Photograph everything. Damage to both vehicles, the scene, skid marks, traffic signals, and any injuries.

- Collect witness names and numbers. Independent witnesses are invaluable.

Within 24–72 hours

- Seek medical attention and keep all records.

- Notify your own insurer that you were in an accident. Do not delay — late notice can jeopardize your claim.

- Report to police if you have not already. A police report number supports your claim.

In the days and weeks following

- Keep a journal of your symptoms, pain levels, and how your injuries affect your daily life.

- Save all receipts for medical costs, prescription drugs, transportation to appointments, and any out-of-pocket expenses.

- Do not post about the accident on social media. Insurers and defence lawyers monitor social media activity.

- Consult a personal injury lawyer before giving a recorded statement to the at-fault driver’s insurer (if they had any) or to any adjuster beyond your own SABs claim.

Our motor vehicle accident team can walk you through the claims process and help you understand the full scope of compensation you may be entitled to.

How Much Compensation Can You Recover?

The amount you may recover depends on your specific circumstances, the severity of your injuries, the coverage available, and which compensation pathway you use. No lawyer can guarantee a specific outcome, but here is a framework for understanding what is typically available.

Statutory Accident Benefits (SABs)

Every injured person — regardless of fault — has access to no-fault accident benefits from their own insurer (or MVACF if uninsured). These include:

- Income replacement benefits (up to 70% of gross weekly income, subject to a weekly maximum under the standard policy)

- Medical and rehabilitation benefits

- Attendant care benefits

- Non-earner benefits for those not in the workforce

- Death and funeral benefits

Enhanced SABs limits (higher income replacement, medical/rehab, and attendant care) can be purchased as optional benefits and can significantly increase the support available after a serious injury.

Tort damages against the at-fault driver

For pain and suffering, you must meet Ontario’s tort threshold — your injuries must be permanent and serious, or meet the definition of a catastrophic impairment under the Insurance Act. If you qualify:

- General damages for pain and suffering

- Loss of income past and future

- Loss of competitive advantage in the job market

- Future care costs

- Family law claims for family members affected by your injury

If the at-fault driver cannot satisfy a judgment (because they are uninsured), OPCF-44R or MVACF may provide recovery up to applicable limits.

To get a preliminary sense of what your claim might be worth, use our personal injury settlement calculator — it takes only a few minutes and gives you a helpful starting point before your consultation.

Why Legal Representation Matters in Uninsured Driver Claims

Uninsured and OPCF-44R claims are procedurally complex. They involve your own insurer in a dual role — as your SABs provider and as the party potentially responsible for the tort gap under OPCF-44R — which creates inherent conflicts of interest.

Common challenges claimants face

- Disputes over whether physical contact occurred in hit-and-run cases

- Insurer arguments that the at-fault driver was actually insured (to avoid the uninsured automobile coverage obligation)

- Undervaluation of damages by adjusters who know the claimant has no identified defendant to sue

- Late notice defences where the insurer argues it was not notified promptly enough

- MVACF procedural hurdles for uninsured victims

What a lawyer can do

An experienced personal injury lawyer can:

- Identify every coverage layer available to you (SABs, DCPD, uninsured automobile, OPCF-44R, MVACF)

- Manage limitation periods and notice requirements so your claim is not lost on a technicality

- Handle the insurer’s adjuster on your behalf

- Retain the right medical experts to document your injuries properly

- Advance your tort claim against the at-fault driver (even if collection is uncertain) while simultaneously protecting your insurer-side claim

- Represent you before the Licence Appeal Tribunal if your accident benefits are denied or disputed

Most personal injury lawyers in Ontario work on a contingency fee basis — meaning you pay nothing unless you recover compensation. There is no financial risk to getting advice.

Talk to a UL Lawyers Team Member

Being hit by an uninsured driver is stressful and confusing — but Ontario law gives you real options. Whether you are navigating an OPCF-44R claim, pursuing accident benefits, or figuring out whether MVACF applies to your situation, the right legal guidance can make all the difference. The team at UL Lawyers offers free initial consultations with no obligation. Reach out to our motor vehicle accident lawyers today — we can review your policy, explain your rights, and help you understand every avenue of recovery available to you.