Receiving a long-term disability denial letter is overwhelming — especially when you are already dealing with a serious illness or injury. The insurer’s decision is not final. In Ontario, you have real options to fight back, but the path forward is technical, deadline-driven, and full of traps that can permanently close the door on your claim if you are not careful.

This guide focuses entirely on what happens after the denial: the appeal mechanics, the deadline windows, how insurers use independent medical examinations to undermine your claim, and the evidence strategies that actually move the needle. If you want background on qualifying for LTD benefits in the first place, our long-term disability practice page covers that foundation. Here, we pick up where the denial letter ends.

Understanding whether to pursue an internal appeal (reconsideration through the insurer) or go straight to a legal claim may be the single most consequential decision you make. Get it wrong and you may forfeit your right to benefits entirely. Read on to understand your choices — and why speaking with a lawyer before doing anything is almost always the right first step.

Table of Contents

- How Do You Appeal a Long-Term Disability Denial in Ontario?

- What Is the Appeal Timeline and Deadline for an LTD Denial?

- How Do IMEs (Independent Medical Examinations) Affect Your Appeal?

- What Evidence Strengthens an LTD Denial Appeal?

- Internal vs. External Appeal: Which Path Is Right for You?

- Common Reasons LTD Benefits Are Denied or Cut Off

- Can You Reverse an LTD Denial After a Failed Internal Appeal?

- How a Lawyer Strengthens Your LTD Appeal Strategy

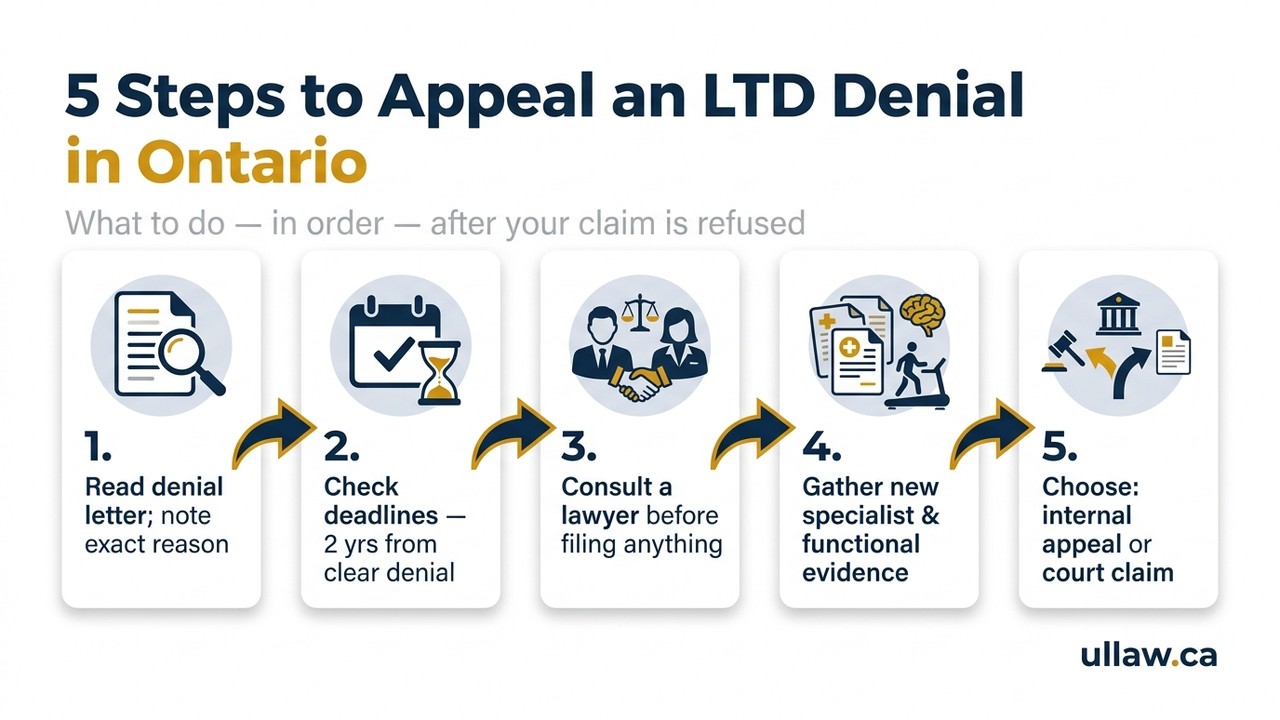

How Do You Appeal a Long-Term Disability Denial in Ontario?

When your insurer denies your LTD claim, their letter will typically outline a process called an internal appeal or reconsideration. This means you submit additional information — updated medical records, specialist letters, functional assessments — and ask the insurer to review its own decision.

Here is the general process:

- Read the denial letter carefully. Identify the exact reason(s) given. Common grounds include failing the “own occupation” or “any occupation” definition of disability, pre-existing condition exclusions, insufficient medical evidence, or a missed proof-of-claim deadline.

- Gather new evidence. A reconsideration without new, compelling evidence rarely succeeds. You need updated records, treating specialist opinions, and ideally functional capacity evaluations.

- Submit your appeal in writing. Always confirm receipt and keep copies of everything.

- Await the insurer’s written decision. Insurers are not bound by strict provincial timelines for reconsideration decisions the way courts are, so follow up regularly.

Alternatively — and this is critical — you may skip the internal appeal entirely and proceed directly to a civil lawsuit in the Ontario Superior Court of Justice. Ontario courts have consistently held that claimants are not required to exhaust internal appeal mechanisms before suing. Your long-term disability lawyer can help you decide which route makes strategic sense in your specific circumstances.

What Is the Appeal Timeline and Deadline for an LTD Denial?

This is where many claimants lose their case before it even starts. Missing a limitation deadline can permanently extinguish your right to benefits, even if your medical evidence is strong.

The Two-Year Limitation Period

Under Ontario’s Limitations Act, 2002, the general limitation period is two years from the date you knew — or ought to have known — that your claim was denied and that a legal proceeding would be appropriate. The clock typically starts running from the date of the denial letter.

Policy Deadlines vs. Statutory Deadlines

Your group or individual insurance policy may contain its own shorter internal deadlines — for example, requiring you to submit an appeal within 60 or 90 days of the denial. These contractual deadlines are separate from the statutory limitation period and can be enforced by the insurer.

The “Clear Denial” Rule

Ontario courts have grappled with cases where insurers send letters that appear to deny benefits but are ambiguously worded. The limitation period generally does not start running until the denial is clear and unequivocal — meaning the claimant understands their claim has been rejected and that litigation would be required. Ambiguous communications can shift when the clock starts, which is why the precise wording of every letter from your insurer matters enormously.

Relief from Forfeiture

Even where a claimant misses a policy deadline, Ontario courts have the power under the Insurance Act to grant relief from forfeiture where the delay was not prejudicial to the insurer and the circumstances are equitable. This is not a safety net to rely on — but it has saved claims that might otherwise have been lost.

The bottom line: treat every denial letter as starting a countdown clock and consult a lawyer immediately.

How Do IMEs (Independent Medical Examinations) Affect Your Appeal?

An Independent Medical Examination (IME) is a medical assessment arranged — and paid for — by your insurer. Despite the word “independent,” these examinations are conducted by physicians selected by the insurance company and are a frequently used tool to build a case against your claim.

How Insurers Use IMEs

- The IME doctor typically spends 60–90 minutes with you — far less time than your own treating physicians have over months or years.

- The resulting report may downplay your symptoms, question your diagnosis, or suggest you can perform work duties inconsistent with your actual functional limitations.

- Insurers routinely cite IME reports as the primary basis for denial or termination of ongoing benefits.

Your Rights Around IMEs

Your policy likely requires you to attend an IME when the insurer requests one. Refusing without legal justification can jeopardize your claim. However, you have the right to:

- Know the name and credentials of the examining physician in advance.

- Bring a support person (though recording is subject to the examiner’s consent).

- Receive a copy of the report.

Countering an Unfavourable IME

The most effective counter to a damaging IME report is a detailed rebuttal from your own treating specialists. Your family physician, psychiatrist, neurologist, or other specialist should respond point-by-point to the IME’s findings. A Functional Capacity Evaluation (FCE) conducted by an independent occupational therapist can also provide objective data that is difficult for insurers to dismiss.

Never treat an IME as routine. Prepare thoroughly, and speak to your lawyer before you attend.

What Evidence Strengthens an LTD Denial Appeal?

A successful appeal almost always turns on the quality and completeness of your medical and functional evidence. Submitting the same records the insurer already reviewed — and rejected — is rarely sufficient.

Medical Evidence

- Specialist opinions from the physicians most qualified to speak to your specific condition (neurologist for MS, psychiatrist for depression and anxiety, rheumatologist for fibromyalgia or lupus, etc.).

- Detailed clinical notes that document your symptoms, functional limitations, and the impact on daily activities — not just diagnoses.

- Diagnostic test results: MRIs, bloodwork, psychiatric assessments, sleep studies, or whatever applies to your condition.

Functional Evidence

- A Functional Capacity Evaluation (FCE) — an objective, multi-hour assessment of your physical and cognitive abilities conducted by a licensed occupational therapist.

- Attending Physician Statements (APS) completed carefully and thoroughly by your treating doctors, addressing the policy’s specific definition of disability.

Vocational Evidence

- A vocational assessment from a certified vocational evaluator can demonstrate that, even if you have some residual capacity, there are no realistic occupations available to you given your education, training, experience, and limitations.

Personal and Collateral Evidence

- A detailed personal affidavit or statement from you describing your daily limitations.

- Statements from family members or caregivers who observe your condition day-to-day.

You can use our long-term disability benefits calculator to get a rough sense of what your monthly entitlement may look like — which can help you understand what is at stake and motivate you to build the strongest possible file.

Internal vs. External Appeal: Which Path Is Right for You?

This is one of the most important strategic decisions in any LTD dispute, and it deserves its own discussion.

Internal Appeal (Reconsideration with the Insurer)

An internal appeal means submitting additional evidence and asking the insurer to reverse its own decision. It is faster and less expensive up front — but it carries real risks:

- You are asking the insurer to overrule itself. Insurers approve a relatively small proportion of reconsiderations.

- You reveal your full evidence strategy before litigation begins. A sophisticated insurer will use your appeal to prepare its legal defence.

- A second denial restarts the clock — but it also means more months without income.

- Internal appeals do not pause the limitation period. If you spend nine months on a reconsideration and then get denied again, you have used up a large portion of your two-year window.

Why Internal LTD Appeals Are Often a Trap

Many claimants pursue internal appeals because the denial letter encourages them to — but that letter is written by the insurer’s claims team, not in your interest. Courts have found that an internal appeal is not a legal prerequisite before suing. In many cases, going directly to litigation preserves more evidence, more leverage, and more time.

External Appeal (Legal Claim / Court Process)

Filing a Statement of Claim in the Ontario Superior Court of Justice sends a clear signal that you are serious. It also:

- Triggers formal discovery, giving you access to the insurer’s internal claims file.

- Allows your lawyer to examine the IME physician and the insurer’s claims handler under oath.

- Opens the door to bad faith damages if the insurer’s conduct was egregious.

A lawyer experienced in plaintiff-side disability insurance litigation can assess your specific policy language, medical evidence, and timeline to recommend which route gives you the strongest chance of success.

Common Reasons LTD Benefits Are Denied or Cut Off

Understanding why your claim was denied is the foundation of your appeal strategy. The most common grounds include:

- Failing the definition of disability. Most policies shift from an “own occupation” definition (unable to perform your job) to an “any occupation” definition (unable to perform any job) after 24 months. Many denials occur at this transition point.

- Insufficient medical evidence. The insurer argues your file does not objectively support the degree of limitation you describe — particularly common in mental health, chronic pain, and fatigue-based conditions.

- Pre-existing condition exclusion. The insurer claims your condition existed before your coverage began and is therefore excluded.

- Failure to comply with treatment. Insurers sometimes deny benefits on the basis that you refused surgery, declined medication, or did not pursue recommended rehabilitation.

- Missed proof-of-claim deadline. Your policy requires you to submit proof of your disability within a specific period. Missing this deadline — even innocently — can trigger a denial.

- Surveillance evidence. Insurers occasionally conduct video surveillance and use footage to argue your functional limitations are overstated.

- Return-to-work cutoff. Benefits are terminated on the basis of a plan to return you to modified or alternative work, even if that plan is unrealistic.

Knowing the specific ground for your denial tells your lawyer exactly what evidence gap needs to be filled.

Can You Reverse an LTD Denial After a Failed Internal Appeal?

Yes — a failed internal appeal does not end your options. Many claimants who are denied at the reconsideration stage go on to successfully resolve their claims through litigation or negotiated settlement.

What Changes After a Failed Internal Appeal

After a second denial, you have a fully documented record of the insurer’s position. Your lawyer can:

- Identify inconsistencies in the insurer’s reasoning across the two decisions.

- Subpoena the insurer’s internal claims notes and communications.

- Challenge the methodology and credentials of the IME doctor in discovery.

- Argue bad faith if the insurer failed to properly investigate, ignored compelling evidence, or applied the wrong definition of disability.

Bad Faith Claims

Under Ontario insurance law and the Insurance Act, an insurer has an obligation to deal with your claim fairly and in good faith. Where an insurer unreasonably denies, delays, or misrepresents the basis for denial, courts can award damages beyond the unpaid benefits — including aggravated and punitive damages in serious cases.

Negotiated Settlements

The majority of LTD disputes that reach the litigation stage settle before trial. Your lawyer can use the strength of your medical evidence and the vulnerabilities in the insurer’s file to negotiate a lump-sum settlement that compensates you for past-due benefits, future entitlement, and — where applicable — bad faith conduct.

The most important step after a failed appeal is to contact a disability insurance lawyer before the limitation period expires.

How a Lawyer Strengthens Your LTD Appeal Strategy

Navigating an LTD appeal without legal representation puts you at a serious disadvantage. Insurers have experienced in-house claims teams and retained legal counsel. You deserve the same level of advocacy.

A plaintiff-side LTD lawyer can:

- Review your policy language to identify the exact definition of disability you must meet and any exclusions that apply.

- Advise on timing — whether to pursue internal reconsideration or proceed directly to litigation based on your deadline position.

- Retain medical and vocational experts to build a file that withstands insurer scrutiny.

- Respond to or challenge IME reports with targeted rebuttal evidence.

- Negotiate directly with the insurer from a position of strength.

- Commence and manage litigation in the Ontario Superior Court of Justice if necessary.

The Law Society of Ontario maintains a public directory of licensed lawyers if you want to verify credentials. Most plaintiff-side LTD lawyers work on a contingency fee basis, meaning you pay no legal fees unless you recover benefits. Always confirm the fee arrangement in writing before proceeding.

Our team at UL Lawyers works exclusively on the plaintiff side — we never represent insurance companies. Visit our long-term disability practice page to learn more about how we can help you, or use our long-term disability benefits calculator to estimate the value of your claim.

Talk to a UL Lawyers Team Member

If your long-term disability claim has been denied — or your benefits have been cut off — you may still have strong options. The team at UL Lawyers represents disabled Ontarians across the GTA and province-wide, always on the plaintiff side. Contact us for a free, no-obligation consultation to discuss your appeal timeline, your evidence, and the strategy most likely to get your benefits reinstated.