When your long-term disability insurer denies or terminates your benefits, it can feel devastating — especially when you know your medical evidence is solid and your condition is real. But some denials go beyond a simple disagreement about the facts. Sometimes an insurer’s conduct is so unreasonable, so careless, or so deliberately unfair that it crosses a legal line. In Ontario, that line is called bad faith.

Bad faith is not just about losing a claim. It is about how an insurer treated you along the way — whether it investigated properly, interpreted your policy honestly, weighed your medical evidence fairly, and communicated with you in a timely and transparent manner. When an insurer fails on those fronts, the legal consequences can extend well beyond repaying the benefits they owe you.

This guide explains exactly what bad faith means in the context of an Ontario long-term disability claim, how insurers commonly breach their duty of good faith, what remedies — including punitive damages — may be available, and how an experienced LTD lawyer can help you hold your insurer accountable. If you have already received a denial and want to know where you stand financially, try our long-term disability benefits calculator as a starting point.

Table of Contents

- What Is Bad Faith in a Long-Term Disability Claim in Ontario?

- What Is the Duty of Good Faith — and What Does It Actually Require?

- What Are the Duties of the Insured (Your Obligations Too)?

- What Are Bad Faith Damages in Ontario — Including Punitive Damages?

- What Is an Example of Bad Faith in an LTD Claim?

- How to Build and Win a Bad Faith LTD Claim in Ontario

- How Does an LTD Lawyer Help With a Bad Faith Claim?

What Is Bad Faith in a Long-Term Disability Claim in Ontario?

Bad faith in an Ontario long-term disability claim means that your insurer did not deal with you honestly, fairly, or reasonably in handling your claim — either when it investigated, assessed, or decided your case.

Every insurance contract in Ontario carries an implied duty of good faith. This duty is not written into most policy documents, but it is imposed by law. It means the insurer must give your claim the same genuine, fair-minded attention it would give its own interests. When it fails to do that, it acts in bad faith.

The duty of good faith is recognized under Ontario’s Insurance Act and has been developed extensively through Canadian common law. Courts have found that insurers occupy a position of significant power over claimants — you cannot simply shop for a new insurer mid-illness — and that power imbalance creates a heightened obligation to act fairly.

What Bad Faith Looks Like in Practice

Bad faith is not a single act. It can be a pattern of conduct. Common examples include:

- Denying a claim without a legitimate reason — citing policy exclusions that clearly do not apply, or ignoring medical evidence that supports your disability.

- Unreasonably delaying benefit payments or decisions without explanation.

- Commissioning a biased Independent Medical Examination (IME) — sending you to a doctor known to produce insurer-friendly reports, then accepting that report over your treating specialists’ opinions without good reason.

- Misrepresenting the policy — telling you that you are not covered when a fair reading of the policy suggests otherwise.

- Failing to communicate — leaving you without updates for months, or not telling you what additional information is needed.

- Repeatedly requesting the same documents that have already been submitted, causing deliberate delay.

- Terminating benefits at the two-year mark (when the definition of disability often changes from “own occupation” to “any occupation”) without conducting a genuine, individualised assessment of your transferable skills, education, and actual job market options.

Not every denied claim is a bad faith claim. Insurers are allowed to investigate, ask questions, and even disagree with your doctor. Bad faith arises when the conduct goes beyond honest disagreement and becomes unreasonable, careless, or dishonest.

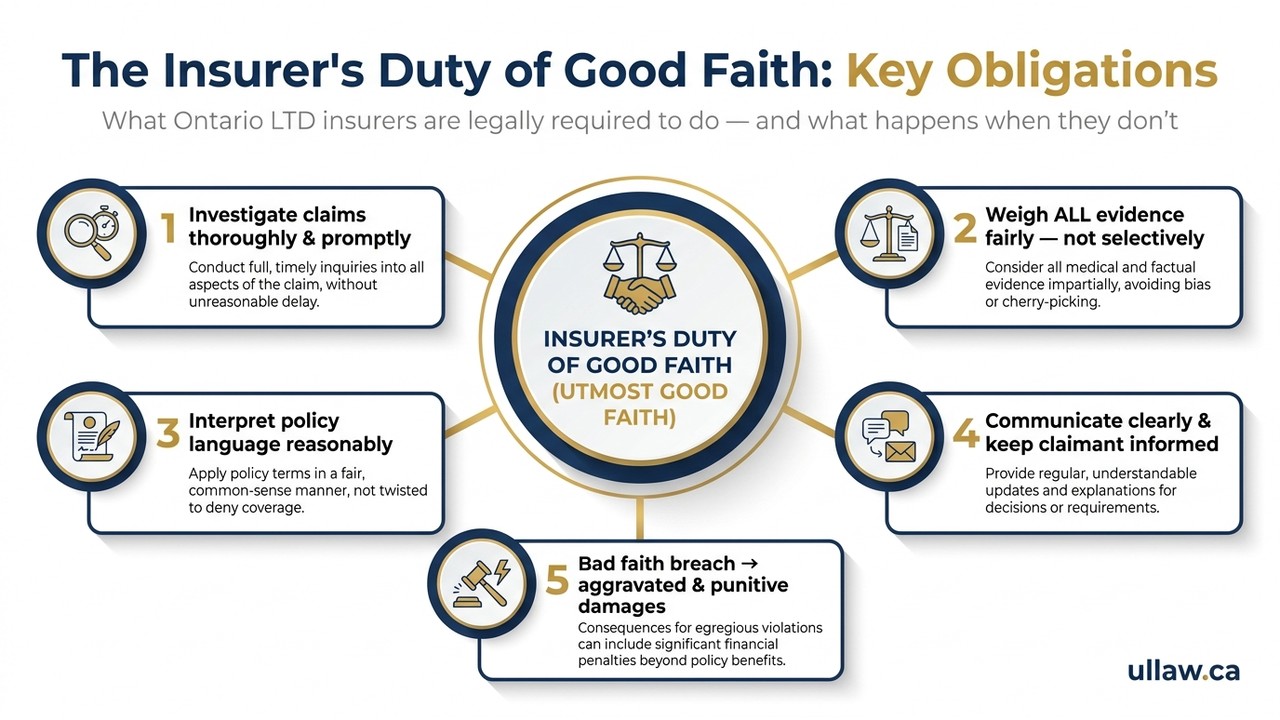

What Is the Duty of Good Faith — and What Does It Actually Require?

The duty of good faith is the cornerstone of every insurance relationship in Canada. It requires your insurer to act fairly and honestly toward you throughout the entire life of your claim — from the moment you file to the final resolution.

This duty is a two-way street, but the insurer’s obligations are especially demanding because of the power imbalance between a large corporation and a sick or injured individual who depends on those benefits to pay rent and buy groceries.

The Insurer’s Core Obligations Under the Duty of Good Faith

Duty to Adequately Investigate

Your insurer cannot make a decision about your claim without first conducting a thorough, genuine investigation. This means obtaining your complete medical records, consulting appropriate specialists, and actually reviewing what it receives. An insurer that denies a claim after a superficial review — or without requesting key medical information — may be found to have breached this duty.

Duty to Assess the Evidence in a Balanced and Reasonable Manner

Once the insurer has the evidence, it must weigh it fairly. That means it cannot selectively focus only on evidence that supports a denial while ignoring, downplaying, or failing to seek out evidence that supports your claim. If your treating psychiatrist, family doctor, and specialist all agree you are disabled, the insurer cannot simply prefer the opinion of a paper reviewer who never examined you — at least not without a compelling, articulated reason.

Duty to Reasonably Interpret the Policy

Insurance policies are dense legal documents. When the language is ambiguous, courts in Ontario apply the principle that ambiguities are resolved in favour of the insured. An insurer that deliberately adopts an unreasonably narrow reading of policy language in order to deny a valid claim is breaching its duty of good faith. Similarly, misrepresenting what a policy covers — whether through negligence or design — is a serious breach.

Duty to Communicate Promptly and Transparently

Your insurer must keep you reasonably informed, tell you clearly what information it needs, and explain its decisions in terms you can understand. Leaving a disabled claimant in silence for months is not only cruel — it may also be actionable.

All of these obligations flow from the overarching principle recognized by Canadian courts and the Law Society of Ontario in its guidance on insurance disputes: the insurance contract is one of the utmost good faith, and that standard runs in both directions.

What Are the Duties of the Insured (Your Obligations Too)?

Good faith is a two-way obligation. While insurers carry the heavier burden, you also have duties as the insured — and failing to meet them can weaken your claim or even give the insurer a legitimate basis for denial.

Your Key Obligations

1. Provide accurate, complete information. When you fill out your application and ongoing claim forms, answer every question honestly. Misrepresenting your symptoms, work history, education, or daily activities — even exaggerating them — can be used against you and may void your policy entirely.

2. Cooperate with the insurer’s reasonable requests. You are required to attend an Independent Medical Examination if your insurer reasonably requests one. You must respond to requests for information and authorizations within a reasonable time. Refusing to cooperate, without good cause, can be treated as a breach of the policy.

3. Continue treatment. Most LTD policies require you to be under the active care of a physician and to follow recommended treatment. If you stop attending appointments or decline reasonable treatment, the insurer may argue your disability is not being properly managed.

4. Report changes in your condition. If your health improves materially, you have an obligation to report that — even if it may affect your benefits.

What You Should NOT Say or Do

A common question is: what not to say to a long-term disability insurer? Here are the key traps:

- Do not minimize your symptoms to sound polite or stoic. Describe your worst days accurately, not your best.

- Do not speculate about returning to work unless your doctor has actually cleared you.

- Do not post on social media in ways that contradict your disability description — insurers do conduct surveillance.

- Do not give a recorded statement without legal advice. You may not be required to, and what you say can be used against you.

Meeting your own obligations also matters strategically: if you have consistently cooperated and the insurer still acted unreasonably, that contrast strengthens your bad faith case.

What Are Bad Faith Damages in Ontario — Including Punitive Damages?

When an insurer is found to have acted in bad faith, Ontario courts can award remedies that go significantly beyond simply paying the overdue benefits. Understanding these remedies is important — they are part of why a bad faith claim can be worth pursuing even when the underlying benefit amounts seem modest.

1. Payment of Benefits Owed

First and most obviously, a successful LTD claim means the insurer must pay all the benefits it improperly withheld, including retroactive payments with interest.

2. Aggravated (Mental Distress) Damages

Aggravated damages compensate you for the mental distress, anxiety, and suffering caused by the insurer’s breach of the duty of good faith — over and above the distress naturally associated with your underlying illness. Courts in Ontario have recognized that disabled claimants are particularly vulnerable, and that an insurer’s unreasonable conduct can cause serious psychological harm. These damages can be meaningful, and they reflect the real cost of living through a bad faith denial.

3. Punitive Damages

Punitive damages are the most striking remedy. They are not about compensating you — they are about punishing the insurer and deterring similar conduct in the future. Canadian courts have awarded punitive damages against LTD insurers when the insurer’s conduct was found to be harsh, vindictive, reprehensible, or malicious.

Punitive damages in insurance bad faith cases in Canada have ranged from tens of thousands to hundreds of thousands of dollars, depending on the egregiousness of the conduct, the insurer’s financial resources, and the need for deterrence. Courts do not award them lightly, but they are a real remedy when the conduct warrants it.

4. Costs

In Ontario civil litigation, a successful plaintiff in a bad faith case may be awarded substantial indemnity costs — meaning the insurer could be ordered to pay a larger portion of your legal fees than in a standard case. This is another tool courts use to express disapproval of particularly unreasonable insurer conduct.

To get a sense of the benefits amount at stake in your own situation, use our long-term disability benefits calculator — knowing the underlying numbers helps your lawyer assess the full picture of what you may be entitled to claim.

What Is an Example of Bad Faith in an LTD Claim?

Concrete examples help make bad faith tangible. Here are realistic scenarios — based on patterns seen in Ontario LTD litigation — that illustrate what bad faith can look like:

Example 1: The Ignored Treating Specialist

A claimant with severe treatment-resistant depression submits reports from her psychiatrist, psychologist, and family doctor, all confirming she is unable to work. The insurer arranges a file review by a doctor who has never examined her and who produces a one-page report saying she should be capable of sedentary work. The insurer terminates her benefits based solely on that paper review, without explaining why it preferred that opinion over three treating specialists. This pattern — dismissing treating physicians in favour of insurer-retained reviewers without proper justification — is one of the most commonly litigated forms of bad faith in Ontario.

Example 2: The Two-Year Definition Switch Denial

A claimant receiving benefits for two years is cut off when the policy shifts from an “own occupation” to an “any occupation” definition of disability. The insurer sends a form letter saying he can do “sedentary work” but never conducts a vocational assessment, never considers his education, age, or the actual job market for his skills, and never speaks to his doctors about functional limitations. Courts have found this type of superficial “any occupation” analysis to be a breach of the duty of good faith.

Example 3: The Surveillance Ambush

An insurer conducts months of video surveillance of a claimant with fibromyalgia, capturing isolated moments of her carrying groceries or walking normally on a good day. It then terminates her benefits without asking her physicians to review the footage or explain it in the context of her fluctuating condition. Using surveillance as a gotcha rather than as one piece of fairly considered evidence — especially without giving the claimant a chance to respond — can ground a bad faith finding.

Example 4: Deliberate Delay

An insurer receives a complete, well-documented claim and then spends eight months requesting documents that have already been submitted, assigning the file to a new adjuster every few weeks, and failing to issue any decision. The claimant, who has no income, falls behind on mortgage payments. Courts take deliberate delay seriously, especially when there is no legitimate reason for it.

How to Build and Win a Bad Faith LTD Claim in Ontario

A bad faith LTD claim is a serious legal undertaking, but it is winnable when the evidence is properly assembled and the legal arguments are carefully crafted. Here is how successful bad faith claims are typically built:

Step 1: Document Everything

From the moment you suspect bad faith, keep a detailed record. Write down every phone call — date, time, who you spoke to, what was said. Save every email and letter. Note every time a document was submitted and every acknowledgment (or lack of one) you received. This paper trail is the foundation of your case.

Step 2: Obtain Your Complete Claim File

You are entitled to request your complete claim file from the insurer. This often reveals internal adjuster notes, supervisor sign-offs, and communications that show exactly how decisions were made — and whether proper procedures were followed.

Step 3: Gather Independent Medical Evidence

If the insurer relied on an IME or paper review to deny your claim, your lawyer will help you obtain independent specialist opinions that directly address and rebut those reports. The strength of your medical evidence is central to both the underlying LTD claim and the bad faith overlay.

Step 4: Identify the Specific Breaches

Bad faith claims are strongest when you can point to specific, documented failures — not just a sense that the insurer was unfair. Your lawyer will analyze the claim file and identify the particular points where the insurer failed its duty to investigate, assess evidence fairly, or interpret the policy reasonably.

Step 5: Quantify Your Damages

Your legal team will calculate not only the overdue benefits and future benefits, but also the aggravated and punitive damages that the insurer’s conduct may warrant. This full picture informs settlement negotiations and, if necessary, litigation strategy.

Step 6: Pursue Resolution — Litigation if Necessary

Many bad faith LTD claims resolve in mediation or negotiation once the insurer understands the full scope of its exposure. If not, Ontario’s civil courts have robust tools to hold insurers accountable. The Ontario courts system provides the forum, and experienced LTD counsel knows how to use it effectively.

For detailed information about your rights and options in an LTD dispute, visit our long-term disability practice page.

How Does an LTD Lawyer Help With a Bad Faith Claim?

Navigating a bad faith LTD claim without legal help puts you at a serious disadvantage. Insurers have in-house legal teams and experienced adjusters. You deserve someone equally skilled in your corner.

What an LTD Lawyer Actually Does

Analyzes your claim file to identify specific breaches of the duty of good faith — not just the denial itself, but how the insurer conducted itself throughout.

Retains independent medical experts who can assess your condition objectively and directly address flawed IME reports or biased paper reviews.

Negotiates from a position of knowledge. An insurer that knows you have a credible bad faith claim — with potential punitive damages exposure — has strong incentives to settle fairly.

Handles all communications. Once you have legal representation, the insurer must deal with your lawyer, not you directly. This immediately changes the dynamic.

Prepares and manages litigation if settlement is not possible — from drafting the Statement of Claim through to trial, if necessary.

Ensures deadlines are met. Ontario limitation periods are strict. Missing a deadline can permanently bar your claim, regardless of its merit. An experienced lawyer tracks every deadline and ensures no procedural door closes on you.

No Upfront Legal Fees

Most Ontario LTD lawyers — including our team at UL Lawyers — work on a contingency fee basis. This means you pay nothing upfront and no legal fees unless and until your case is successfully resolved. This arrangement ensures that access to justice does not depend on your financial situation — which matters enormously when your disability benefits have been cut off and money is tight.

We Serve All of Ontario

Whether you are in Burlington, Toronto, Hamilton, Ottawa, Windsor, Thunder Bay, or anywhere else in the province, our team can help. LTD disputes are handled provincially, and we represent clients across all of Ontario. Many consultations and case management steps can be completed remotely, so geography is rarely a barrier.

If you are dealing with a denied or terminated LTD claim and suspect your insurer has not dealt with you fairly, learn more about your options on our long-term disability practice page.

Talk to a UL Lawyers Team Member

If you believe your long-term disability insurer has not dealt with you fairly — whether through an unjustified denial, unreasonable delay, a biased IME, or a failure to properly assess your evidence — you may have a bad faith claim worth pursuing. Contact UL Lawyers for a free, no-obligation consultation. Our team serves clients across Ontario, works on a contingency fee basis so there is nothing to pay upfront, and has no bad questions — only answers. Reach out today to find out where you stand.