When your insurer decides whether to approve or deny your long-term disability (LTD) claim, one thing matters more than almost anything else: the quality and completeness of your medical evidence. Yet most claimants submit whatever paperwork their doctor hands them — and then receive a denial letter they were never prepared for.

Insurance companies employ medical reviewers, independent medical examiners (IMEs), and file analysts whose job is to find gaps in your evidence. A missing diagnosis code, a vague physician note, or a functional capacity form left half-blank can be enough to justify cutting off your income. The burden is on you — the claimant — to prove that your condition prevents you from working.

This guide breaks down the specific documents and reports that build a compelling LTD file, explains how insurers attack medical evidence, and shows what you can do when your claim has already been denied. If you want to understand how much you might be entitled to while you read, our long-term disability benefits calculator can give you a quick estimate. For personalised legal support, visit our long-term disability practice page.

Table of Contents

- What Medical Evidence Is Needed for a Long-Term Disability Claim?

- The Role of Medical Evidence in LTD Claims

- Types of Medical Evidence: From Chart Notes to Functional Capacity Evaluations

- What Conditions Qualify for Long-Term Disability in Canada?

- Quality of Medical Evidence: What Insurers Look For (and Attack)

- Independent Medical Examinations: What to Know Before You Go

- What Not to Say to Long-Term Disability Insurers

- Common Reasons LTD Claims Are Denied — and How Evidence Can Fix Them

- How an LTD Lawyer Helps You Build and Protect Your Medical Evidence

What Medical Evidence Is Needed for a Long-Term Disability Claim?

At its core, a successful LTD claim rests on a clear, consistent, and objective paper trail that connects your diagnosis to your functional limitations — and those limitations to your inability to work.

Insurers in Ontario are regulated under the Insurance Act and the policy contract itself. Most group LTD policies require you to prove disability through “satisfactory proof” submitted to the insurer. What that phrase means in practice:

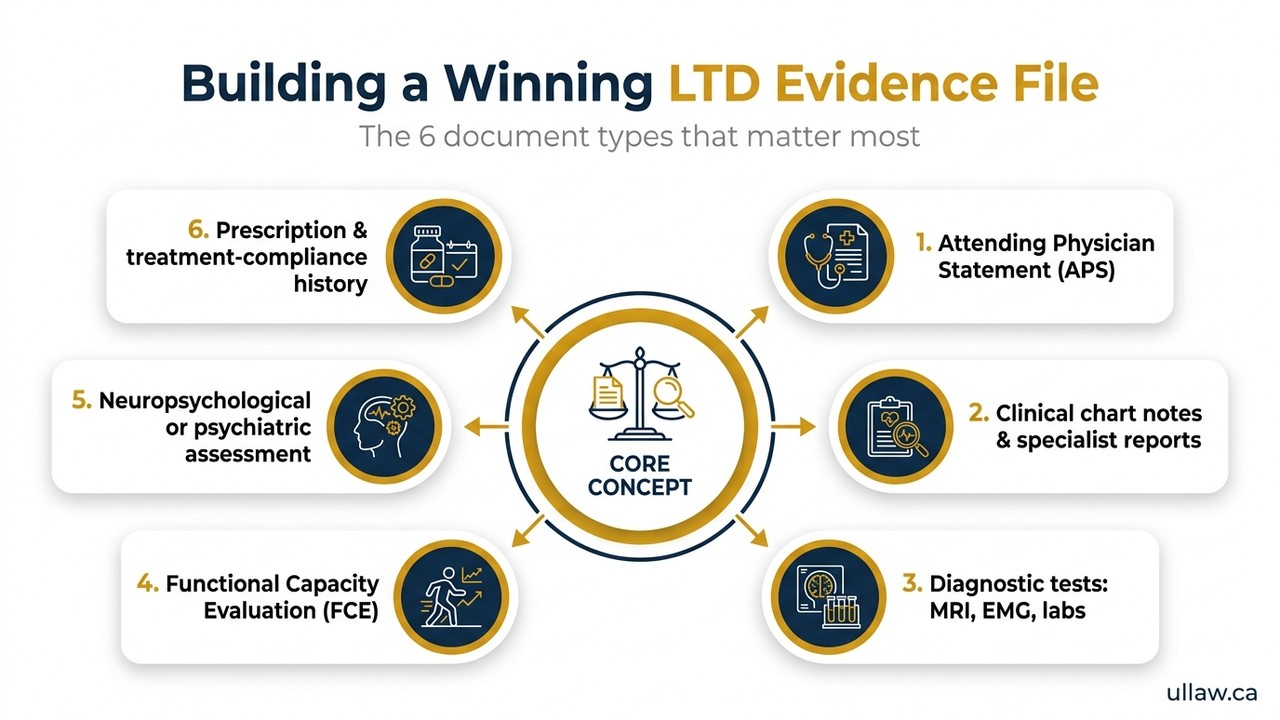

The Core Evidence Package

- Attending physician’s statement (APS): The single most important document. Your treating doctor must describe your diagnosis, symptom severity, treatment plan, prognosis, and — critically — your functional limitations (sitting, standing, lifting, concentrating).

- Clinical chart notes: Raw office visit notes dating back to the onset of your condition. Insurers look for the frequency of visits and consistency of reported symptoms.

- Diagnostic test results: Lab work, MRI/CT/X-ray reports, nerve-conduction studies, sleep studies, blood panels — whatever objectively confirms your condition.

- Specialist reports: Letters and consultation notes from rheumatologists, neurologists, psychiatrists, physiatrists, or any specialist relevant to your condition.

- Hospital records: Emergency department visits, in-patient admissions, and discharge summaries show severity.

- Prescription history: A documented medication record confirms active, ongoing treatment.

- Mental health records: For psychiatric conditions (depression, anxiety, PTSD), therapy session notes, psychiatrist assessments, and any hospitalisation records are essential.

Why Completeness Matters More Than Volume

Insurers do not reward claimants who submit more paper — they reward claimants who submit coherent paper. Every document should tell the same story: you have a diagnosed condition, it causes specific functional limitations, and those limitations prevent you from performing your job (or any job, depending on the policy’s definition of disability after the initial qualifying period).

If your chart notes say “patient reports improvement” but your APS says “totally disabled,” the insurer will seize on the inconsistency. Work with your treating physicians to ensure records accurately reflect your worst and most representative days, not just the days you pushed through to attend an appointment.

The Role of Medical Evidence in LTD Claims

Medical evidence does not just open the door to LTD benefits — it keeps that door open throughout the entire claim lifecycle.

At the initial application stage, the insurer uses your evidence to decide whether you meet the policy’s definition of disability during the own-occupation period (typically the first 24 months), when you must prove you cannot do your specific job.

At the 24-month definition change, the standard shifts. Most policies then require proof you cannot perform any occupation for which you are reasonably suited by education, training, or experience. Your medical file must evolve to meet this higher threshold — new specialist reports, updated functional assessments, and current treatment records all become critical.

During ongoing claim review, the insurer may request updated evidence every 6–12 months. Gaps in treatment — missed appointments, discontinued medication — are routinely used as a reason to terminate benefits.

At the appeal or litigation stage, your complete medical file becomes the evidentiary record that either supports or undermines your case. Courts and adjudicators look at the totality of clinical documentation, so every record matters.

In short: medical evidence is not a one-time submission. It is a living record you and your healthcare team must actively maintain.

Types of Medical Evidence: From Chart Notes to Functional Capacity Evaluations

Different types of evidence serve different functions in your LTD file. Understanding what each does helps you ask the right questions of your healthcare providers.

Treating Physician Statements

Your family doctor or specialist completes the insurer’s Attending Physician Statement (APS) form. This form typically asks for:

- Primary and secondary diagnoses (with ICD codes)

- Date of onset and first treatment

- Current symptoms and their severity

- Physical and cognitive restrictions and limitations

- Prognosis and expected duration of disability

Tip: Ask to review the completed APS before it is submitted. Vague answers like “see chart” or “moderate limitations” without specifics give the insurer room to dispute your claim.

Functional Capacity Evaluations (FCEs)

An FCE is a structured, multi-hour assessment conducted by an occupational therapist or physiotherapist that objectively measures what you can and cannot do physically. It tests:

- Lifting, carrying, pushing, and pulling tolerance

- Sitting and standing endurance

- Hand grip strength and dexterity

- Positional tolerances (bending, reaching, crouching)

An FCE commissioned by your healthcare team — rather than the insurer’s — can be a powerful rebuttal to an insurer’s claim that you are capable of sedentary work.

Neuropsychological Assessments

For cognitive disabilities (brain injury, fibromyalgia fog, severe depression, MS), a neuropsychological assessment documents deficits in memory, concentration, processing speed, and executive function — areas insurers routinely dismiss as subjective.

Pain and Fatigue Questionnaires

Validated tools like the Brief Pain Inventory, Fatigue Severity Scale, or DASH questionnaire give standardised, peer-reviewed weight to symptoms that are otherwise hard to quantify.

Mental Health Documentation

Psychiatric and psychological records deserve special attention. Insurers frequently challenge mental health claims as subjective. Strong documentation includes:

- Formal DSM-5 diagnoses from a psychiatrist or registered psychologist

- Structured assessment tools (PHQ-9 for depression, GAD-7 for anxiety, PCL-5 for PTSD)

- Therapy session progress notes showing ongoing, consistent impairment

- Any records of hospitalisation or crisis intervention

What Conditions Qualify for Long-Term Disability in Canada?

There is no fixed government list of conditions that automatically qualify for LTD benefits. Unlike the Canada Pension Plan Disability benefit — which has its own federal eligibility criteria — private and group LTD policies focus on functional impairment, not diagnosis alone.

That said, conditions that frequently support successful LTD claims in Ontario include:

- Musculoskeletal disorders: Chronic back pain, degenerative disc disease, rheumatoid arthritis, fibromyalgia

- Mental health conditions: Major depressive disorder, severe anxiety, PTSD, bipolar disorder

- Neurological conditions: Multiple sclerosis, Parkinson’s disease, epilepsy, neuropathy, traumatic brain injury

- Cardiovascular conditions: Heart failure, post-cardiac event recovery, arrhythmias

- Cancer: Active treatment and post-treatment fatigue and side effects

- Autoimmune conditions: Lupus, Crohn’s disease, ulcerative colitis

- Chronic pain syndromes: Complex regional pain syndrome (CRPS), failed back surgery syndrome

Does Neuropathy Qualify for Disability?

Yes — peripheral neuropathy can qualify for LTD benefits, but the key is documentation. Neuropathy must be supported by nerve-conduction studies or electromyography (EMG) results, specialist reports from a neurologist, and an APS that connects the nerve damage to specific functional limitations (inability to stand, operate equipment, maintain grip, etc.).

What Is the Hardest Disability to Prove?

Claims involving “invisible” conditions — fibromyalgia, chronic fatigue syndrome (ME/CFS), chronic pain, and psychiatric disorders — are routinely the most contested. These conditions lack definitive objective tests. Winning such claims requires layered evidence: specialist diagnoses, validated symptom scales, FCEs, neuropsychological testing, and consistent treatment histories that collectively paint an undeniable picture of impairment.

Quality of Medical Evidence: What Insurers Look For (and Attack)

Submitting records is not enough — the quality and persuasiveness of those records determines the outcome.

What Strengthens Your File

- Consistency: Symptoms described the same way, visit after visit, over months or years

- Objectivity: Hard data from tests, imaging, and standardised scales rather than purely subjective complaints

- Specialist involvement: A family doctor’s APS carries less weight than a specialist’s detailed opinion

- Functional specificity: Statements like “patient cannot sit for more than 20 minutes without pain escalation” beat “patient has back pain”

- Treatment compliance: Evidence you have followed every recommended treatment shows good faith and rebuts suggestions that you could improve if you tried

How Insurers Attack Medical Evidence

Insurers use several tactics to undermine even strong files:

- Selective reading: Highlighting one positive chart note while ignoring dozens of negative ones

- IME ambush: Sending you to an independent medical examiner chosen and paid by the insurer, whose report may minimise your impairments — see the next section

- Surveillance: Video or social media monitoring looking for activity inconsistent with claimed limitations

- “Insufficient proof” letters: Requesting document after document, then claiming you failed to provide satisfactory evidence

- Transferable skills analysis: Arguing that even if you cannot do your old job, you could do some other sedentary role

Being aware of these tactics is the first step to countering them.

Independent Medical Examinations: What to Know Before You Go

If your insurer requests that you attend an Independent Medical Examination (IME), do not treat it as a routine appointment. The examiner is retained by the insurance company, and their report often becomes the centrepiece of a denial.

Your Rights at an IME

- You are generally required to attend reasonable IMEs under your policy, but the insurer cannot demand unlimited examinations

- You may bring a support person to observe (not participate)

- You are entitled to receive a copy of the IME report

- You have the right to have your own physician review and rebut the IME report in writing

How to Prepare

- Do not minimise your symptoms. Describe your worst typical day, not your best day

- Be consistent with everything you have told your treating doctors

- Do not perform activities beyond your genuine functional capacity just to appear cooperative

- Make a written note of everything that happens during the examination immediately afterward

Counter the IME With Your Own Evidence

A well-documented FCE or neuropsychological report from your team can directly challenge an unfavourable IME finding. Courts have repeatedly recognised that insurer-retained IME reports deserve no more automatic weight than evidence from a claimant’s own treating practitioners.

What Not to Say to Long-Term Disability Insurers

What you say — and write — to your insurer can be used against you. A few common mistakes:

- “I’m doing better.” Even a polite, social response to an adjuster’s wellness question can be recorded and used to suggest your condition has improved. Stick to factual descriptions of your functional limitations.

- “I did [physical activity] last weekend.” Insurers may use casual statements about activity — even gardening or driving — to argue you are not as limited as claimed. You are not required to volunteer information beyond what is asked.

- Inconsistent descriptions of your condition. Always describe your disability in the same terms you use with your doctor. Inconsistency — even innocent exaggeration or understatement — is used to attack your credibility.

- Delaying or refusing treatment. Saying you have not tried recommended therapy or medication gives the insurer grounds to argue your disability is not as severe as claimed, or that it is treatable.

- Posting on social media. Photos or check-ins showing physical activity are regularly used in surveillance. Privacy settings offer limited protection — assume anything you post can be found.

When in doubt, consult a lawyer before responding to insurer requests for recorded statements or detailed personal questionnaires.

Common Reasons LTD Claims Are Denied — and How Evidence Can Fix Them

Understanding why claims are denied points directly to the evidence you need to fix them.

| Denial Reason | Evidence That Addresses It |

|---|---|

| “Insufficient medical evidence” | Updated APS, specialist reports, recent diagnostic tests |

| “Condition is not totally disabling” | FCE, neuropsychological assessment, pain/fatigue scales |

| “IME contradicts your physician” | Written rebuttal from treating specialist, second independent FCE |

| “You can perform sedentary work” | Vocational report, cognitive testing showing concentration deficits |

| “Lack of ongoing treatment” | Documented treatment plan, specialist referrals, therapy records |

| “Pre-existing condition exclusion” | Timeline of diagnosis vs. policy effective date; legal advice on policy interpretation |

Denials are not the end of the road. Most group LTD policies have an internal appeal process, and if that fails, you may have a right to pursue the insurer in Ontario civil court. The Ontario Courts handle LTD breach-of-contract claims, and limitation periods are strict — typically two years from the date of denial under the Limitations Act, 2002. Do not wait.

How an LTD Lawyer Helps You Build and Protect Your Medical Evidence

Gathering medical evidence sounds straightforward — but most claimants don’t know what is missing until after they receive a denial letter.

An experienced LTD lawyer can:

- Audit your existing file to identify gaps before submission or appeal

- Brief your treating physicians on the legal standard of proof and what language makes an APS persuasive vs. dismissible

- Retain independent experts — FCE assessors, neuropsychologists, vocational consultants — who understand what courts and insurers expect

- Challenge IME reports with targeted written rebuttals from your own medical team

- Manage insurer correspondence so nothing you say inadvertently undermines your claim

- Pursue litigation if the insurer refuses to honour a valid claim

Most LTD lawyers in Ontario work on a contingency fee basis — meaning you pay nothing upfront and legal fees come only from a successful recovery. This makes legal help accessible even when your income has been cut off.

For a fuller picture of the LTD process in Ontario — from application to appeal — visit our long-term disability practice page. To get a rough sense of what your monthly benefits could look like, try our long-term disability benefits calculator.

The Law Society of Ontario also maintains a referral service if you want to verify a lawyer’s credentials before retaining them.

Talk to a UL Lawyers Team Member

Ready to review your LTD file? At UL Lawyers, we offer a free, no-obligation consultation to claimants across Ontario — whether you are preparing an initial application, facing a denial, or heading into an appeal. Contact us today and let us help you build the medical evidence record your claim deserves.